Until 2019 Austrian municipalities followed the rules of cameralistic system. The budgeting and also accounting was done according to a cash-flow oriented system. From the beginning of 2020 an accrual system consisting of three perspectives must be implemented. The income statement (Ergebnishaushalt) shows the resource flows within the municipality. The cash flow statement (Finanzierungshaushalt) shows the cash inflows and outflows. The balance sheet statement (Vermögenshaushalt) includes balances of property, accounts receivable, accounts payable, loans etc. With this shift to a resource oriented concept a holistic assessment of municipal households is possible.

The introduction of the new accrual accounting system in Austria as of 2020 made it necessary to implement a major relaunch of the platform. In fact, Open Spending Austria has been completely rewritten and redesigned.

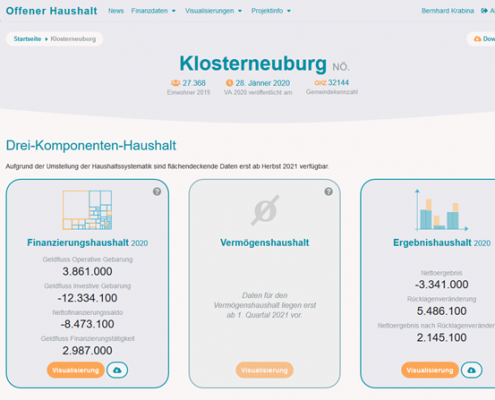

City of Klosterneuburg at Open Spending Austria: https://www.offenerhaushalt.at/gemeinde/klosterneuburg

As data currently is only available in for the planned budget of 2020, only two of the three budget components can be visualized (see figure). The two components already available are the cash flow statement (left) and the income statement (right) For the third component (middle, the balance sheet statement), data from the actual spending 2020 will be needed that will be available as of spring 2021.

Currently, more then 1.100 municipalities in Austria have disclosed their spending data on the platform, which is more then 53 percent. And more are joining every month…