This post is the third in a short series that GIFT is running to provide ideas for countries preparing their next Action Plans. The first two blogs looked at what steps countries should take to increase fiscal transparency in their next Action Plans; and how transparent and participatory budgets and budget processes are currently in OGP countries. The posts draw on a series of GIFT papers, ˜Fiscal Transparency in Open Government Partnership Countries, and the Implementation of OGP Commitments: An Analysis’, prepared for successive meetings of the OGP-Fiscal Openness Working Group, and on GIFT case studies of public participation in fiscal policy.

Summary:

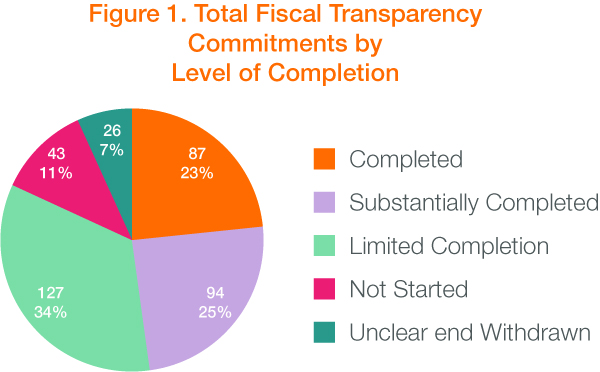

Commitments on fiscal transparency made up around one-third of all the commitments in the first fifty-one OGP Action Plans. The IRM reports assessed that implementation of 87 fiscal transparency commitments (23%) was completed, 94 (25%) were substantially completed, 127 (34%) were assessed as limited completion, 69 (18%) were not started, unclear or withdrawn. These results are broadly similar to the results for implementation of all commitments. Of those countries with more than five fiscal transparency commitments, notable progress in implementing the commitments was made by Croatia, Mexico, Brazil, Indonesia, Moldova and the Philippines. GIFT is working pro-actively through the OGP-Fiscal Openness Working Group to encourage and support more ambitious, well-specified, and well-implemented commitments on fiscal transparency and participation in the next round of Action Plans.

How many fiscal transparency commitments were in the first generation of OGP Action Plans?

This post uses data in the first 51 IRM reports to look at how well countries have implemented their fiscal transparency commitments. Progress in implementing commitments is assessed both in the aggregate – compared to implementation of all OGP commitments – and on a country-by-country basis.

GIFT defines fiscal transparency commitments as commitment that deal with any aspect of government revenues, expenditures (including on public services), financial or non-financial assets or liabilities – including any activities that involve public participation in policy development or implementation in these areas.

By this definition, there was a total of 378 commitments in the first 51 Action Plans, which was 33% of all the commitments in those Plans. These 378 commitments included 74 ˜star commitments’ “ commitments that combined three elements: clear relevance to OGP goals; assessed as likely to be moderate to high impact; and assessed as having been substantially completed or completed. Star commitments made up 20% of all fiscal transparency commitments, a little lower than the 25% share of star commitments in all OGP commitments.

There was a very wide range in the share of fiscal transparency (FT) commitments in each country’s total commitments, from none (Chile, Panama, and Romania) to 100% (Guatemala).

How well did countries implement their FT commitments?

Figure 1 illustrates the level of completion of FT commitments, using data extracted by GIFT from the executive summaries of the first 51 IRM reports.

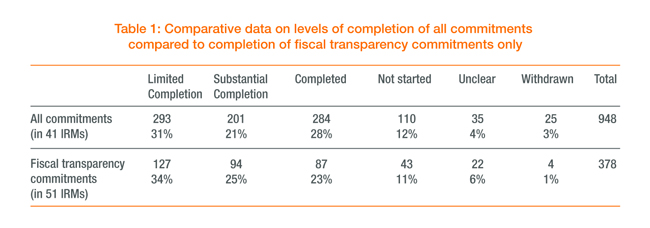

Table 1 presents comparative data for levels of completion of FT commitments (above) against the same data for all commitments (from analysis by the OGP Secretariat (Foti) from just the first 41 IRM reports). The results are broadly similar, given the margins of error in these exercises, particularly for the percentage of commitments either completed or substantially completed (48% c.f. 49%).

{kind=link}

Which countries had the best record of implementing their FT commitments?

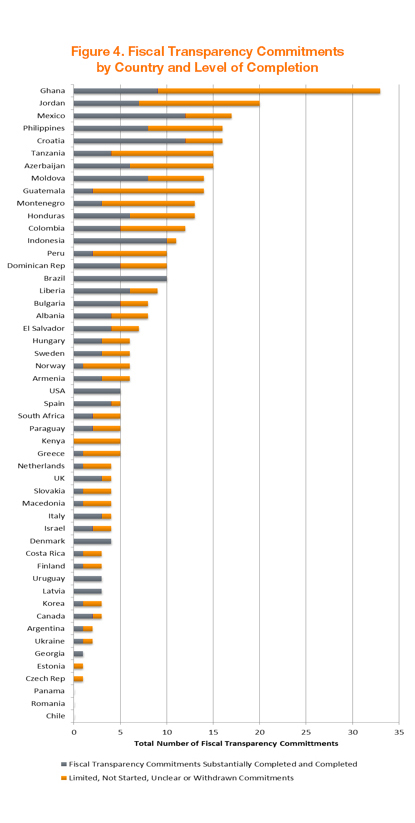

Turning to levels of completion at the country level, Figure 4 presents data extracted by GIFT from the same 51 IRM reports.

The first point to note about Figure 4 is that GIFT has re-defined some detailed FT sub-commitments as commitments for the purposes of this analysis, in order to make cross-country comparisons more meaningful. This is because the definition of a commitment varies widely within and across Action Plans.

For example, Croatia’s first Action Plan contained only nine commitments, considerably less than the average number of commitments (which was 22 in the first 41 OGP Action Plans). However, the first commitment in the Croatia Action Plan covered four discrete and significant elements: publication of the budget proposal, of monthly budget reports, of a semi-annual report, and of an annual budget report. These four sub-components, each of which is more substantive than some commitments in other Action Plans, have been defined for this analysis as four separate commitments. Similarly, the Ghana Action Plan had 13 commitments but 48 discrete sub-commitments, and the latter number was used in this analysis of commitments.

Bearing this in mind, the following points can be seen from Figure 4:

- The weightiest FT reforms are found in those OGP countries with both a significant number of FT commitments and a high rate of implementation. Of those countries with more than 5 FT commitments, notable progress was made by:

- Croatia “ 12 out of 16 FT commitments completed or substantially completed.

- Mexico “ 12 out of 17 FT commitments completed or substantially completed.

- Brazil “ 10 out of 10 FT commitments completed or substantially completed.

- Indonesia “ 10 out of 11 FT commitments completed or substantially completed.

- Moldova “ 8 out of 14 FT commitments completed or substantially completed.

- The Philippines “ 8 out of 16 FT commitments completed or substantially completed.

- A small number of countries achieved over 90% completion or substantial completion of their FT commitments, including Indonesia, Denmark, Georgia, Latvia, Brazil, Honduras, Uruguay and the USA.

At the country level the stand-out performer on FT star commitments was Croatia (11 star commitments) “ note again that the number of star commitments has been redefined as above for all commitments, to improve cross-country comparability. Honduras, Moldova, Colombia, and the Dominican Republic also had an impressive number of star commitments (5-6 each), while Ghana had 4. It needs to be noted that the star commitment rating was created only after the cohort 1 countries (the founding eight OGP members) prepared their first Action Plans.

What is not clear from the data is the extent to which commitments represent new initiatives or were based on pre-existing activities or policies. This reduces the ability to compare the ambition of commitments across countries.

Where to next?

In conclusion, fiscal transparency commitments make up a large portion of all OGP commitments, although the proportion of fiscal transparency commitments and how well they have been implemented varies widely from country to country. GIFT is working pro-actively through a number of channels to encourage and support more ambitious, well-specified, and well-implemented commitments in the next round of Action Plans. The first post in this series outlined our suggestions for new FT commitments that countries should consider including in their next Action Plans. The OGP-Fiscal Openness Working Group is bringing together ministry of finance officials and CSO experts to work collaboratively in peer to peer discussion and learning on the critically important agenda of increasing the accountability and effectiveness of the management of public resources. Please contact us if you would like to find out more about or to engage with the Fiscal Openness Working Group.

Murray Petrie -Â GIFT Lead Technical Advisor